You decide to refinance your Colorado home.

Your new loan estimate arrives.

You see title fees again and feel confused.

Many homeowners ask the same core question; Do I need title insurance when refinancing my mortgage? The answer depends on the type of policy and your new loan.

This guide explains how title insurance works during a refinance. It also shows when your existing coverage still helps you and when lenders require new protection. Along the way, you will see how Hera Title supports refinance closings in Colorado.

What Title Insurance Does When You Buy Or Refinance

Title insurance protects against covered problems with legal ownership. These problems can hide in public records. Examples include old liens, recording errors, or missing signatures.

The American Land Title Association notes that title insurance protects homeowners for as long as they own the property, in exchange for a one time premium at closing.

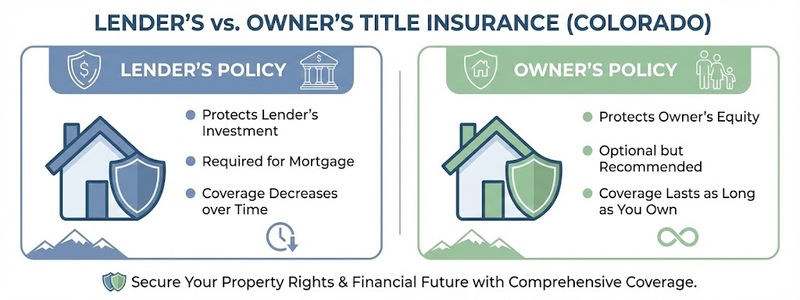

Most transactions involve two policies:

- A lender policy that protects the lender’s interest.

- An owner policy that protects your ownership interest.

Want a quick visual refresher before you read further? You can watch our short video introduction to title insurance then return for more details here.

Lender Policy vs Owner Policy During A Refinance

A refinance replaces your old mortgage with a new loan. The loan balance, rate, or lender often change. Your actual ownership usually does not.

Because the loan changes, lenders almost always want a new lender title policy. The policy must match the new loan amount and date. It protects the lender if a covered title problem appears after closing.

Your owner policy works differently. It usually:

- Connects to your ownership, not a single loan.

- Stays in force while you still own the property.

- Continues through multiple refinances, subject to policy terms.

So during a typical refinance:

- The lender orders a new lender policy.

- Your existing owner policy often continues to protect you.

For specific details, review your old closing documents with a title professional. They can confirm how your policy works.

Do I Need Title Insurance When Refinancing?

Now we can answer the main search question more directly. Do I need title insurance when refinancing if I already paid for it once?

In most refinance situations in Colorado:

- Yes, your lender will require a new lender title policy.

- No, you usually do not buy a brand new owner policy, because you already have one.

The new lender policy reflects the new loan and date. It gives the lender confidence that the title remains clear after the last closing.

Your owner policy still matters. It can protect your equity if someone later claims an interest in your property, within policy limits.

If you never bought an owner policy during your original purchase, ask about options now. Some situations allow discounts or special pricing when you add coverage during a refinance. Federal discussions note that many refinances involve reissue rates or discounts based on earlier policies.

How Title Insurance Affects Refinancing Closing Costs

Refinancing closing costs can feel like alphabet soup. Title charges form only one part, but they stand out.

Common title related items include:

- Title search or title examination

- Settlement or closing fee

- Lender title insurance premium

- Endorsements requested by the lender

- Recording fees for new documents

The Consumer Financial Protection Bureau explains that title service fees usually appear in sections B or C of your Loan Estimate and Closing Disclosure. These forms also show whether you can shop for those services.

Because costs vary, it helps to compare quotes. You can ask one or two Colorado title companies for estimates using the same loan amount and location. Then review those quotes with your lender.

Remember, the cheapest line item does not always equal the best experience. Careful title work helps protect both your home and your refinance.

Why Title Companies Recheck Your Title During A Refinance

Years often pass between your purchase and your refinance. During that time, new issues can appear in public records.

Examples include:

- A contractor lien that never got released

- A judgment recorded against an owner

- Unpaid property taxes or association dues

- Boundary or easement questions

The title company searches the records again to spot these problems. The lender wants a clear report before funding the new loan. You also benefit from another review of your property’s legal history.

Industry and government discussions highlight how closing costs, including title services, have risen in recent years. Updated searches help ensure that these costs still deliver real protection.

Colorado Considerations For Refinance Title Insurance

Title practices differ across states. Colorado has its own regulations and customs. Counties also handle recording in their own ways.

A Colorado consumer advisory notes that title insurers in the state compete on both price and service. It encourages homeowners to compare premiums and ask about discounted rates.

That advice applies during a refinance as well. You can:

- Ask your lender whether you may choose the title company.

- Compare quotes from at least two Colorado providers.

- Ask each company to explain any special refinance pricing.

Local expertise matters. A team that works every day with Douglas, Arapahoe, or El Paso County records may solve issues faster.

How Hera Title Supports Refinance Closings In Colorado

Refinancing should feel manageable, not stressful. Hera Title focuses on clear communication and efficient refi closings for Colorado homeowners.

When you choose Hera Title, you can expect:

- Plain language explanations. The team explains lender and owner policies without jargon.

- Transparent quotes. You receive a clear breakdown of title services, insurance, and fees.

- Local knowledge. The staff understands Colorado regulations and county recording offices.

- Flexible signings. You can often choose between in office or mobile options.

Hera Title’s real estate title services cover title search, examination, closing coordination, and issuance of both lender and owner policies.

Whether your home sits in Castle Rock, Greenwood Village, or another Front Range community, Hera Title aims to keep your refinance smooth and well organized.

Questions To Ask Before You Refinance

Before you lock your new rate, ask a few focused questions.

Ask your lender

- Will this refinance require a new lender title policy?

- Can I choose my own title company for this loan?

- When will you send the title order to the company?

Ask your title company

- Did I receive an owner policy at my original closing?

- Does that owner policy still protect me after this refinance?

- Which title fees can I control or compare?

- When will you share my final closing figures?

These questions help you understand the real role of title insurance. They also clarify do I need title insurance when refinancing in my specific situation.If you live in Colorado and plan a refinance, you can contact Hera Title with these questions today. The team will review your needs, coordinate with your lender, and guide you through each step of the closing process.